Homework H20

Implicit Volatilities?

Learning Goals

Creating financial charts from data retrieved from a remote database.

Context

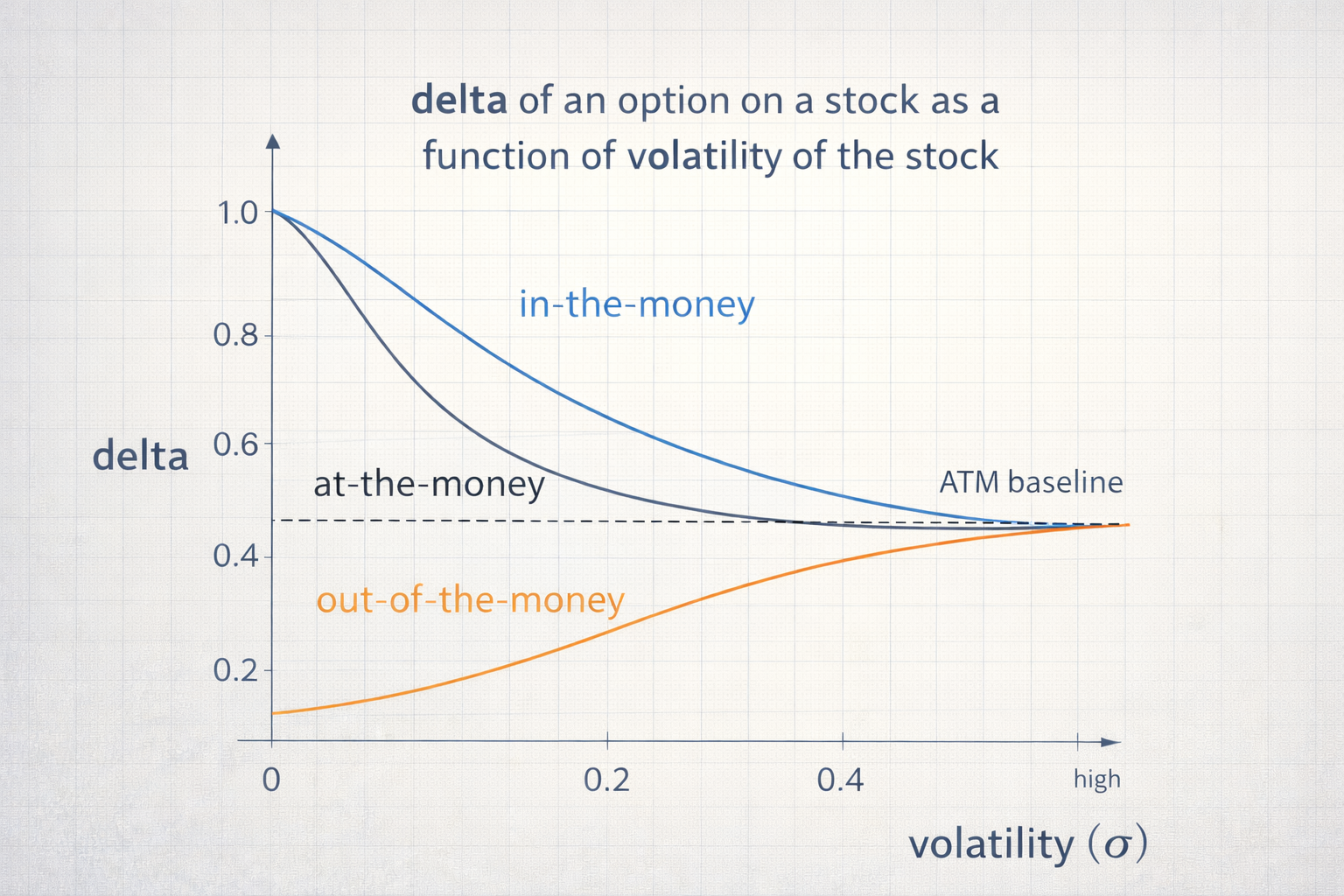

“Have you figured out how to estimate the volatilities?”

Ms. Tradewell has appeared at your desk again. Always practical, always thinking a few steps ahead. “You will need them soon,” she

continues, “to calculate the deltas and therefore the trade sizes.”

For a fraction of a second, you consider confessing your complete ignorance on the subject. But before you can say anything, Mr. Bonds

interjects. “MOST ASSUREDLY, Goldie! We will employ an implicit method to extract volatility estimates from current market conditions.”

He gestures confidently toward your screen. “For now, we will compute point estimates and assume volatility is constant. Later, we will

build a real-time estimator that continuously updates those values as market data evolves.”

Ms. Tradewell nods once. “Ah. Implied volatilities. Good. Glad you are thinking ahead.” She turns and walks away.

A brief silence follows.

You look at Mr. Bonds. “Thank you, Mr. Bonds. That was a timely and most needed save.”

He waves it off casually. “Implied volatility was the topic of my doctoral dissertation. I even built a tool to estimate it directly from

market data. Use it to evaluate the volatilities for our initial basket of stocks.”

You stare at the screen, digesting what you have learned.

Mr. Bonds has a PhD in Finance to back up all that bombast.

And he codes.

It is a good day. For once, you do not have to build a new module yourself.

Task

This homework cannot be done until the new tickers (the one chosen by the class), are inserted in the Databases.

Using the tool, estimate the volatilities of the 12 stocks that we will use in the Hedge Tournament.

Report your results using this workbook. Zip it with the note (if you submit as a

team) as H20.zip

Criteria/Requirements

The closer you are to the true values, the higher the grade.

Hints and Tips

- This homework requires DB access (= you may not use the big Shumway lab and most of RRH 300).